The Fiscal Weight of Monetary Policy

The logic of central bank independence is being overrun by unconventional monetary policy

Recently, the Governor of the Bank of England has been citing gilt yields as evidence that the government must control its borrowing. In an FT interview on 1 June, Bailey said the surge in 10-year yields “did show the importance of balanced public finances” and that “people can take a message from the market”. But this is a strange argument coming from the Bank. The Bank of England is the only major central bank currently actively undertaking quantitative tightening (QT), which, by adding to the supply of long-dated gilts, pushes their prices down and yields up. The Monetary Policy Committee's (MPC) interest rate decisions determine the short end of the curve. And even the residual component, conventionally read as market judgment of fiscal credibility, is not independent of the Bank, because the market prices gilts based on expectations of how the Bank will respond to the actions of the elected government. These yields then become the item that the Bank cites against it. So the Bank is, in effect, invoking the consequences of its own operational choices as proof of the necessity of fiscal restraint.

The architecture of independence

In 1998 the Bank of England Act gave the Bank operational independence over interest rate decisions, with the goal of keeping inflation at a target set by Parliament. When it came to the Bank’s operating costs, the arrangement rested on three institutional features: (1) These costs, while ultimately drawn from the Treasury, were funded through a stable mechanism called the Cash Ratio Deposit Scheme (a precursor to the 2024 Bank of England Levy), which meant that in principle (if not in practice) the Bank’s operations were funded through its own income, specifically, the interest earned on its own balance sheet assets. (2) The balance sheet itself was small and slow-moving. (3) The costs associated with overnight rate-setting, while funded by the Treasury, had only indirect, marginal, slow-moving fiscal consequences. These were transmitted through the price of newly issued gilts rather than through the adjustment of existing operational cash flows.

The logic was that operational independence was contingent on financial independence. A central bank dependent on year-by-year Treasury appropriations faces implicit pressure on its policy choices regardless of formal mandate. The point is made explicitly in the European Central Bank’s reading of Article 130 of the Treaty on the Functioning of the European Union, and implicitly in Cukierman, Webb and Neyapti’s foundational index, and in successive HM Treasury reviews of the CRD scheme and the Bank of England Levy that replaced it, where the existence of a self-funding mechanism distinct from Treasury appropriation is where that principle is at work.

Pre-financial crisis this architecture held. And it held even after the 2006 reform introduced remuneration on small operational reserve balances, to refine the Bank's control over short-term rates in what is now known as the corridor system. The interest paid on £20 billion worth of reserves stock across the system sat comfortably within the Bank's own funding capacity. The Treasury was financially entangled with the Bank, through coupons on the gilts the Bank held and the return of any surplus, but this entanglement did not vary materially with the Bank’s choices. Its balance sheet operations were short-term and self-reversing, producing no large discretionary fiscal flows. The 1998 separation was, in those conditions, approximately real.

Quantitative easing and a new era

The crisis, and QE in particular, changed this arrangement. Between 2009 and 2022, the Bank's holdings of gilts rose from essentially nothing to nearly £900 billion at peak. To obtain those gilts, the Bank created reserves on a corresponding scale. The reserves stock across the banking system rose from around £20 billion to almost £1 trillion. The corridor system was not workable at this scale, and the Bank moved to a floor system in which the Bank Rate is paid on the full stock of reserves.

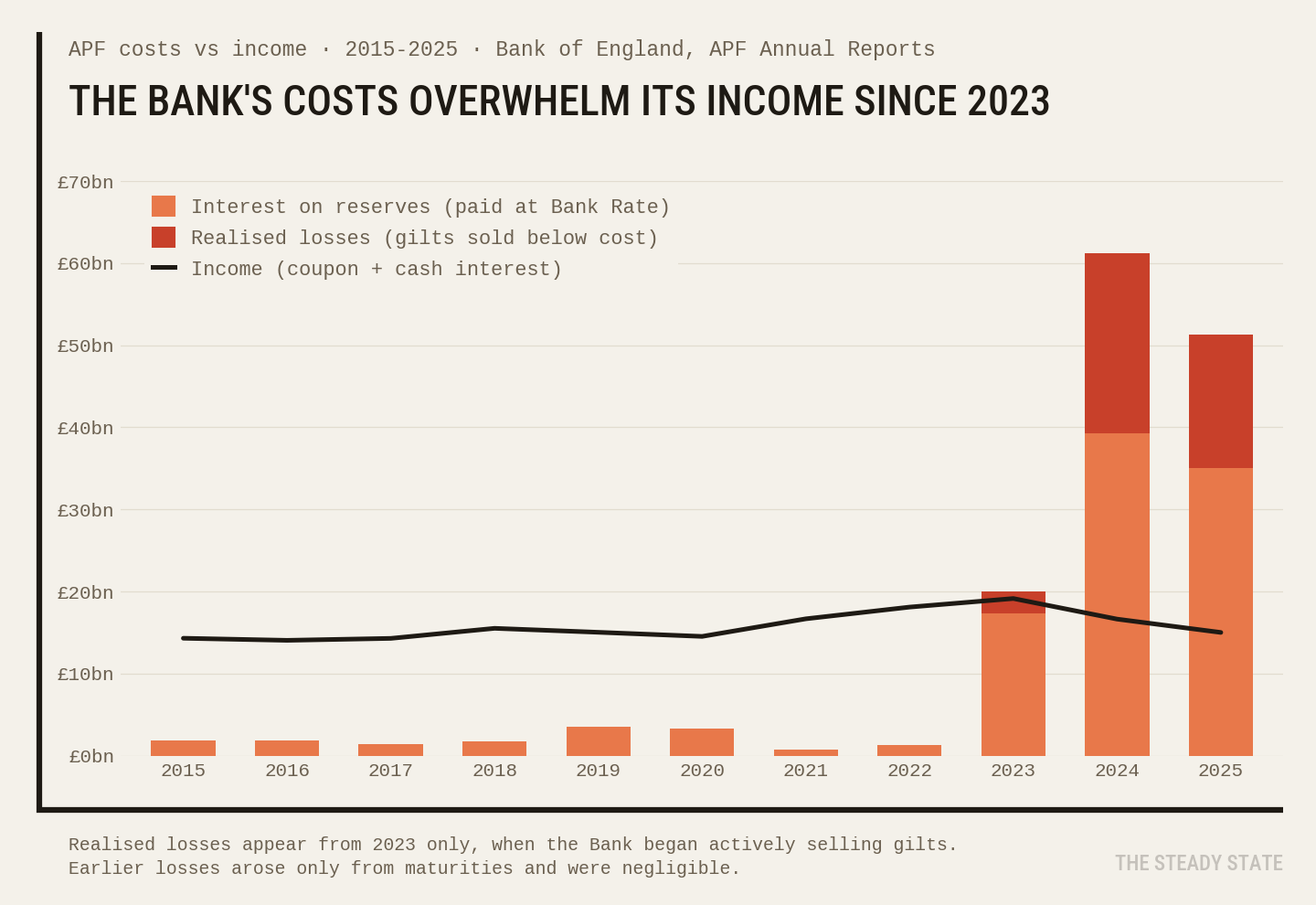

When the Bank Rate is low, that floor system continues to fall within the Bank’s own sources of income. But, when the Bank Rate rises to 5.25 per cent (as it did in 2023) and the reserves stock is still above £700 billion, the gross interest bill on reserves alone can exceed £35 billion a year. That is well beyond the Bank's own funding capacity. This fact tests the financial independence premise under which the architecture of the 1998 framework was constructed.

This may seem like a transitional problem, assuming that the peculiarity of the QE and the QT cycles will eventually pass and things will return to ‘normal’. But it would serve us to recognise that we are in a different macroeconomic world from the one before 2008. Each crisis since then has required some form of unconventional intervention, be it QE, the Special Liquidity Scheme, term funding schemes, the temporary Ways and Means extension during the Covid pandemic, the emergency gilt purchases of September 2022 and so on. And each intervention sets an institutional precedent.

The changing times were formally recognised in February 2025, when the Treasury and the Bank jointly published an updated Memorandum of Understanding (MoU), which governs the financial relationship between these institutions. The framework set out is far from the lean separation envisaged in 1998. What was presented instead was an architecture for joint operation, with explicit protocols for sharing risk, formal capital principles, and indemnity arrangements for "unconventional monetary policy asset purchases." The MoU now describes arrangements that will form part of the next non-orthodox episode in whatever form it takes.

Blurred lines of monetary and fiscal policy

When the Asset Purchase Facility (APF) was set up in 2009, an exchange of letters between Chancellor Alistair Darling and Governor Mervyn King authorised the first round of QE. As the Bank faced large potential losses and limited capital, it was arranged that the Treasury would indemnify those losses in return for receiving any profits. The arrangement was framed at the time as a one-off backstop necessary to make QE possible in the urgent conditions of 2009.

And yet, as the 2025 MoU was finalised, the Governor's own letters frame the indemnity as the mechanism that continues to enable the Monetary Policy Committee to take its decisions. Independence now depends on Treasury underwriting, with the magnitude of the settlement determined by the Bank's choices, rather than agreed in advance.

Someone might defend this by arguing that the indemnity is just accounting. The Treasury would have been paying coupons on the gilts the APF holds anyway; in that sense, the indemnity simply reroutes a cost that would still exist had the Bank not engaged in asset purchases. That is partly true, but the difference is that the Treasury used to know its coupon costs years in advance. Now, not just the margin, but a substantial portion of its ongoing costs, depend on whatever Bank Rate the MPC sets at any given moment.

The architecture is also a choice, but the choice is not between fiscal and non-fiscal arrangements. At this scale, central bank operations inevitably have fiscal outcomes. Paying Bank Rate on reserves is a transfer to the holders of those reserves, whoever absorbs the cost. The choice is about how these fiscal flows are recorded. The Federal Reserve records losses as a deferred asset on its own balance sheet, absorbing them out of future profits, with no immediate fiscal flow to the Treasury. The Bank of Japan retains losses on its balance sheet for long periods. The UK alone transfers those fiscal flows directly to the Treasury, so that monetary operations are recorded in fiscal accounting in real time. The UK arrangement is therefore more transparent than the alternatives. But that transparency translates those flows into immediate political pressure on a government bound by fiscal rules to keep the headline accounts balanced. The elected government does not make decisions on monetary operations, yet it is politically accountable for the accounts those flows shape. When one institution's choices impact the operational and political constraints of another, whose decisions take priority and whose are treated as residual has constitutional consequences for democratic government.

Andrew Bailey’s Times op-ed offers reassurance: "the overall cost of the Bank's QE and QT operations is broadly neutral". But "broadly neutral" rests on the Bank's chart of the cumulative net fiscal impact in present-value terms across the programme's full 60+ year lifetime. Even if one accepts the methodology on which this claim rests, citing the net position over 60 years sidesteps the real issue. At the recent scale, the Bank’s decisions can materially disrupt or support fiscal policy in any given year. The 1998 settlement held because the Bank's limited remit made its operations not only narrow but predictable enough for the Treasury to plan around; these operations now put the Treasury in an increasingly reactive position. The losses since late 2022 are concentrated within the current political cycle, not spread across the window over which Bailey claims neutrality.

Independence has drifted into dominance

The original concern that motivated independence was that political pressure would flow into the Bank. The fear was that elected politicians, facing short-run electoral incentives, would press for monetary policy more accommodating than long-run stability required. Whether one agrees with that premise or not, what has emerged is the opposite. The pressure now flows out of the Bank, into fiscal policy. Bank Rate and QE/QT decisions determine gilt yields. The cost of servicing both new debt and existing reserves is set by the Bank. The Bank then cites these as evidence that the government must restrain itself.

Paul Tucker, the former Deputy Governor of the Bank, argues in his 2018 book Unelected Power that delegation to non-democratic bodies is legitimate only under specific conditions: a precisely defined mandate, accountability proportionate to the powers delegated and, critically, that the independent agency must not be making “big choices on distributional trade-offs“ or decisions that “materially shift the distribution of political power”1. The Bank's operations have drifted far beyond what such criteria would allow. The toolkit of forward guidance, QE and QT, alongside macro-prudential regulation and banking supervision, operates on the Bank's own discretion within a broad framework rather than under specific authorisation. And these tools, exercised at the current scale, produce precisely the consequences Tucker's criteria exclude: distributional trade-offs between asset-holders and non-asset-holders, and material shifts in political power away from the elected government.

QT was begun under the MPC’s own initiative, with no Chancellor's letter pre-authorising its scale or pace (the Treasury’s approval in this instance has been retrospective, confirming the APF size after the MPC had decided how fast to reduce it). The September 2022 gilt interventions, taken under a broad financial stability mandate, were similarly discretionary, and so were their removal the following October. The mandate is wide enough to accommodate both intervention and refusal to intervene within a very short period of time.

As Tucker warned, accountability has been diffuse. The political costs of those decisions now routinely fall on the elected government, which bears the institutional consequences of choices the Bank makes. The Bank’s actions in 2022 and in the run-up to it did not go unscrutinised. Questions were raised about the use of QT, about the inadequate oversight of LDI pension funds’ hedging strategies, and about their indirect subsidy through gilt purchases. The House of Lords Economic Affairs Committee conducted a review of operational independence at its 25-year mark and called for reforms. But none of this translated into institutional consequences for the Bank. Truss became the shortest-serving Prime Minister in UK history, Kwarteng lost his job, and the fiscal direction was immediately reversed under a new Chancellor brought in to restore market confidence. The mechanisms of accountability worked when it came to parliament. But the Bank’s Governor and MPC, whose decisions also shaped the conditions of the episode, continued in their roles unchanged.

What follows

The current arrangement, in which a delegated body exercises substantial discretionary power across multiple policy domains, without specific authorisation for its operations and without commensurate political accountability, violates the principle that grounds the framework’s own legitimacy.

There is a broader question of whether the framework was the right institutional answer to the problems it was designed to address. That is a question for another piece. The fact is the framework, by its own logic, no longer operates as it was intended to operate. On those grounds, the Bank can no longer be treated as entirely independent of the elected government. Continued legitimacy for the Bank’s arrangements requires, at the very least, either democratic authorisation of operations whose fiscal consequences cross some threshold, or a formal commitment to coordination between monetary and fiscal authorities commensurate with the scale of what now passes between them.

Paul Tucker, Unelected Power: The Quest for Legitimacy in Central Banking and the Regulatory State (Princeton University Press, 2018), p. 569 (Appendix).

I think Daniela Gabor is on the same page...

"A Bank of England moment is long overdue -

the Bank has become an unaccountable vigilante of fiscal orthodoxy, run by conservative monetarists, actively destroying fiscal space despite pleas from investors, politicians and academics"

https://x.com/DanielaGabor/status/2076611419735314623

Patricia, good blog. I have to confess I have thought the BoE mandate needed revision for some time but the scale of the QT operations & the fiscal costs underlines the need for greater democratic control & oversight not less.